How will the Federal Budget affect you?

During this year’s Federal Budget announcement Treasurer Josh Frydenberg stated

“Australia is back!”. The Budget proposes positive changes to superannuation, an extension

of the low and middle income tax offsets and a boost to aged care services.

Summary

We’ve summarised some of the key points from the Budget below but, remember, these are subject to the passing of legislation:

• From 1 July 2022, if you’re aged 67 to 74 you will

not be required to meet the work test to make

non-concessional contributions and salary sacrifice

contributions to super

• From 1 July 2022, you can make downsizer super

contributions if you’re age 60 and over (currently

you need to be age 65 or over).

• From 1 July 2022, if you’re a first home buyer you

can release up to $50,000 (up from $30,000) from

your voluntary super contributions to help you buy

your first home.

• The low and middle income tax offset is to extend

to the 2021/22 financial year with a maximum offset

of up to $1,080 for individuals or $2,160 for a couple.

• Additional support for elderly Australians requiring

care either within the home or in a residential aged

care facility.

Superannuation

The work test for older Australians From 1 July 2022, if you’re aged 67 to 74 you will not be required to meet the work test to make non-concessional contributions and salary sacrifice contributions to super. The work test will still be required to make personal deductible contributions to super.

What is the work test?

The work test means you have been gainfully employed for at least 40 hours in 30 consecutive days during the financial year of the contribution.

The announcement also proposed that individuals aged 67 to 74 will also be able to access the non-concessional bring forward arrangement. This is subject to contribution cap eligibility.

Downsizer super contributions

From 1 July 2022, you can make downsizer super contributions if you’re age 60 and over (currently you need to be age 65 or over).

Downsizer super contributions allows you to contribute a maximum of $300,000 (for each eligible member of a couple) to super up to the total proceeds from the sale of your home.

Superannuation for low income earners

From 1 July 2022, if you receive employment income of less than $450 per month your employer will now be required to pay you the superannuation guarantee (SG). The Retirement Income Review estimates that, approximately 300,000 additional people will receive superannuation guarantee payments each month, of whom 63% are women.

Changes to the First Home Super Saver scheme

From 1 July 2022, if you’re a first home buyer you can release up to $50,000 (up from $30,000) from your voluntary super contributions to help you buy your first home. Under the scheme, voluntary concessional and non-concessional contributions made on or after 1 July 2017 may be released from super to help you purchase your first home. Currently, you can release up to $15,000 of voluntary contributions from any one financial year, up to a total of $30,000 in contributions across all financial years, plus earnings on those voluntary contributions. Under the proposed changes, you will be able to release up to

$15,000 of voluntary contributions from any one financial year, up to a total of $50,000 contributions across all financial years, plus earnings.

Relaxing residency requirements and legacy pensions for SMSFs and SAFs

From 1 July 2022, if you have a self-managed super fund (SMSF) or small APRA fund (SAF) with old complying pensions (including term allocated or market-linked pensions) you will be able to exit these legacy pensions. For some SMSFs the cost of running these pensions has been more than the actual pension

they receive. Additionally, the residency rules for SMSFs will be relaxed so that you can be a non-resident for five years before affecting the SMSF residency rules. The ‘active member test’ will be removed for both SMSFs and SAFs.

Small and medium business owners

If you are an eligible small or medium business owner, you will be able to deduct the full cost of eligible assets incurred between 7.30pm (AEDT) on 6 October 2020 and 30 June 2023. This was due to end on 30 June 2022.

This applies to businesses with an aggregated annual turnover or total income of up to $5 billion.

The depreciating asset must be:

• new or second-hand (if it is a second-hand asset, aggregated turnover must be below $50 million)

• first held at, or after, 7.30pm (AEDT) on 6 October 2020

• first used, or installed ready for use, between 7.30pm (AEDT) on 6 October 2020 and 30 June 2023.

The temporary loss carry-back has also been extended by one year. This entitles eligible businesses to carry-back tax losses from the 2022/23 financial year to offset previously taxed profits in a prior financial year starting from the 2018/19 financial year through to the 2021/22 financial year.

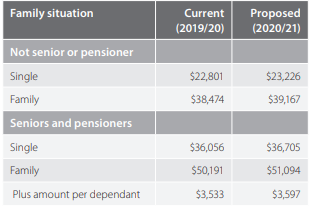

Indexation of Medicare levy thresholds

The Government is proposing to increase the Medicare levy

thresholds for singles, families, seniors, and pensioners from

1 July 2020.

Social security and housing

Increased child care subsidies

From 1 July 2022, child care subsidies paid to approved child care providers will increase, further reducing the cost of child care fees for families.

Current child care subsidy

The maximum child care subsidy payable is 85% of child care fees.

The same rate applies per child in care.

Families with a combined annual income above $189,390 have

a child care subsidy cap of $10,560 per child, per year.

New child care subsidy

A maximum subsidy of 95% of child care fees will apply to the

second and any subsequent child in care for families with more

than one child aged five and under in child care.

Abolish the child care subsidy cap of $10,560 per child per year.

Improvements to the Pension Loan Scheme

Accessing lump sums

From 1 July 2022, you will be able to access lump sum advance payments from the Commonwealth under the Pension Loan Scheme (PLS). Up to 50% of the maximum annual rate of Age Pension can either be paid as a single lump sum or two instalments within a year.

Currently, the PLS allows combined pension and loan payments up to 1.5 times the maximum pension rate, paid fortnightly.

It doesn’t allow access to lump sums. To qualify, you or your partner must own real estate in Australia that can be used as security for the loan.

Modernising tax residency

The Government is proposing to simplify the individual tax residency rules, replacing the existing ‘resides’ test with a ‘183 day’ test. This test is similar to residency tests in place for New Zealand and the United Kingdom.

Under this test, anyone who is physically present in Australia for at least 183 days during a financial year will be taken to be an Australian tax resident.

Simplifying self-education expense deductions

The Government has proposed to simplify self-education expense deductions. Currently the first $250 is excluded from being deductible. It is proposed that this ‘first $250 exclusion’ be removed. This change will allow individuals to claim the full amount of any self-education expenses incurred in a financial year.

Extension of First Home Loan Deposit Scheme

The Government has proposed two extensions to the First Home Loan Deposit Scheme.

Family Home Guarantee

From 1 July 2021, if you are a single parent with dependants you may be eligible to build a new home or buy an existing home with a home loan deposit of 2%. It will be available to both first home buyers and previous owner-occupiers. You must be an Australian citizen, at least 18 years of age and have an annual

taxable income of no more than $125,000.

New Home Guarantee

If you are a first home buyer looking to build a new home or purchase a newly-built home In 2021/22, you may be eligible to do so with a deposit of as little as 5% (lenders criteria apply) and you will not need to take out Lenders’ Mortgage Insurance because of guarantees provided by the Government.

Aged care

Improving aged care

The Government’s response to the Royal Commission into Aged Care Quality and Safety is a five-year reform plan based on the following five pillars:

• Home care – an additional 80,000 Home Care Packages will be released over two years.

• Support to aged care providers to deliver better care and services, including food, through a new government-funded basic daily fee supplement of $10 per resident per day.

• Introduction of a new star rating system to highlight the quality of aged care services.

• Create a single assessment workforce to undertake all assessments that will improve and simplify the assessment

experience for senior Australians as they enter or progress within the aged care system.

• Updating the Aged Care Act and establishing new governance and advisory structures.

If you would like to discuss any of the above Budget topics or would like further information, please contact our office.

Leave A Comment