An article by Shane Oliver;

Share markets remained under pressure last week but I remain of the view it’s unlikely we’re sliding into a grizzly bear market as conditions aren’t in place for recession in the US, globally or Australia

US shares fell 3.8%, Eurozone shares lost 1.6%, Japanese shares fell 0.2%, Chinese shares fell 3.5% and Australian shares declined 0.3%. Reflecting the “risk off” tone bond yields fell, credit spreads widened and commodity prices fell, with the oil price down another 11% over the last week, leaving it down 34% from its high in early October. The $US rose slightly and this weighed on the $A.

Shares retesting October lows – double bottom or resumption of the slump? Share markets fell back to around their October lows over the last week. A retest of the lows is quite normal after the sort of fall we saw in October. Whether markets form a double bottom and head back up or break decisively lower to new lows is unclear.

In favour of the former, less stocks have made new lows into the latest fall and Asian and emerging markets are looking a lot healthier (having led this share slump and having had much deeper falls). But against this, many of the triggers for the fall in markets remain in place. The bottom line is that I don’t know whether it will remain just a correction or maybe slide deeper into what I like to call a gummy bear market (where markets have a 20% top to bottom fall but are up a year after the initial 20% decline). But I remain of the view it’s unlikely we are sliding into a deep or grizzly bear market as the conditions are not in place for recession in the US, globally or Australia.

Potential triggers to watch for a rebound include a meeting at the G20 meeting between Presidents Xi and Trump in the week ahead, more signs of a possible Fed pause on interest rates and a stabilisation/improvement in growth indicators outside the US. In terms of the Trump/Xi G20 meeting, the APEC debacle between the US and China and a report by the US Trade Representative repeating criticism of China are driving low market confidence of a deal being reached between the US and China. However, against this, Trump appears to want a deal, knowing that further tariff hikes (which are really tax hikes) will start to offset his fiscal stimulus next year and may be starting to impact business confidence and hence capital spending. All of which may start to negatively impact Trump’s 2020 re-election prospects. Reports that White House trade adviser and protectionist Peter Navarro won’t be attending the meeting is also a positive.

On the petrol front

While the 34% plunge in the oil price since early October is weighing heavily on energy shares, it’s positive for growth going forward and hence an eventual recovery in share markets. Lower oil prices help take pressure off inflation and put discretionary spending power back into the hands of households. So far it’s a saving of around $11 a week for a typical Australian household but this could increase, as the fall in oil prices flows through with a lag to lower petrol prices.

Along with the high likelihood of more income tax cuts (which could be announced in next month’s mid-year budget review), this means that despite falling house prices, it’s not all doom and gloom for consumer spending in Australia. Further falls in world oil prices may be limited though as OPEC is likely gearing up to cut production at its December 6 meeting.

Source: Bloomberg, AMP Capital

What’s happening in Italy?

Italy looks to be heading into what is called an Excessive De

ficit Procedure – a process administered by the European Commission but approved by Eurozone finance ministers, designed to get its expansionary budget deficit back on track with debt limits – but a major crisis still looks unlikely. More likely is some sort of fudge combining various delays in enforcing any deficit reduction and some compromises. The rest of Europe won’t want to put too much pressure on Italy for fear of fuelling anti-Euro sentiment, and in any case, by the time Italy has to respond to any requests under the EDP it won’t be till later next year by which time the 2019 budget will be largely history.

What’s happening in the US?

US economic data was on the soft side. Home building conditions fell sharply in October, albeit catching down to other housing-related indicators, housing starts and existing home sales rose but are trending sideways, underlying capital goods orders were soft, leading indicators were weak in October, with the falling share market acting as a drag and business conditions PMIs fell slightly in November, albeit they remain strong. Naturally, the weakness in housing indicators raises memories of the GFC but note that housing inv

estment is running at a relatively modest 3.9% of GDP and hasn’t kept up with demographic demand, in contrast prior to the GFC when it reached 6.7% of GDP and was way ahead of demographic demand. While you can get hurt falling out of high rise, you are less likely to get hurt falling out of the ground floor.

And Down Under?

RBA Governor Lowe’s comments in the past week were particularly significant for two reasons. Firstly, he looks to be becoming more concerned about credit tightening in saying that “a few years ago credit standards were way too loose, there has been a correction of that, but I am starting to be a bit concerned the pendulum might be swinging a bit too far the other way.”

Second, he also acknowledged the risks around wages remaining weak, even if unemployment falls further: “I suspect nationally we could sit at [an unemployment rate] around 4.5 per cent without seeing wage growth pick up by too much”.

He is clearly aware that estimates putting the so-called NAIRU at 5% are rubbery. Perhaps he is starting to question the RBA’s own mantra that the next move in rates is more likely up than down.

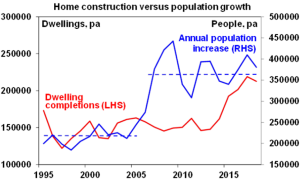

Lower immigration levels on the way?

There is always a debate going on about the appropriate level of immigration in Australia, but this has been mainly outside the major political parties or on the fringe of them. PM Scott Morrison changed all that in the last week flagging a cut to the annual immigration cap of 190,000 by 30,000. At present, this sounds like just affirming the actual level of immigration, which has already slowed by about 30,000. So, no big deal. But having brought the debate into the centre of politics risks seeing immigration getting cut further, given angst about the issue particularly in Melbourne and Sydney. This is particularly relevant to the property market as it was the surge in population growth from around mid-last decade without a housing supply pick up (until around 2015) that has played a big role in the surge in house prices relative to incomes.

Yeah, yeah, yeah, the surge in credit, speculation, foreign demand, etc, also played roles too. But the point is that if immigration starts to fall back at a time of rising supply, it will be one more factor sending property prices south in Sydney and Melbourne (which take something like 60% of immigrants) – along with tighter credit, rising supply, a significant pool

of borrowers having to switch from interest only to principle and interest mortgages, reduced foreign demand, fears around tax changes reducing future investor demand, etc. Our view remains that these two cities will see 20% top to bottom price declines out to 2020 but there are clearly some risks on the downside to this.

Source: ABS, AMP Capital

Keep an eye on these this week

The big event this will be the meeting between Presidents Trump and Xi on the sidelines of the G20 meeting (Friday & Saturday) in Buenos Aires to discuss trade.

In the US, the focus is likely to be on the Fed. While the minutes from the last Fed meeting (Thursday) will likely confirm that it remains upbeat and on track to raise rates again in December, another speech by Fed Chair Powell (Wednesday) is likely to repeat that he is aware of the various headwinds to the US economy, leaving the impression that the Fed is open to a pause on interest rates next year. Of particular interest will be what, if anything, he has to say about continuing share market volatility and recent softness in housing and business investment indicators. On the data front, expect home price data (tomorrow) to show continuing modest gains, consumer confidence for November (also tomorrow) to show a slight fall from 18-year highs, new home sales (Wednesday) to show a bounce, September quarter GDP growth (also Wednesday) to be revised up slightly to 3.6% from 3.5%, personal spending growth (Thursday) to have remained solid but with core private consumption deflator inflation falling back to 1.9% year on year.

In Australia, speeches by RBA Governor Lowe and Assistant Governor Kent today will be watched for any clues on rates. On the data front, expect to see a 1% gain in construction data for the September quarter (Wednesday), a 1.5% gain in September quarter business investment (Thursday) and continuing moderate credit growth (Friday) with ongoing weakness in lending to investors. A key focus will be whether investment intentions data points to further improvement.

Outlook for markets

Shares remain at risk of further short-term weakness, but we continue to see the trend in shares remaining up, as global growth remains solid helping drive good earnings growth and monetary policy remains easy.

Low yields are likely to drive low returns from bonds, with Australian bonds outperforming global bonds as the RBA holds and the Fed continues to hike (albeit they may slow down a bit).

Having fallen close to our target of $US0.70, the Australian dollar is at risk of a further short-term bounce, as excessive short positions are unwound. However, beyond a near-term bounce, it likely still has more downside into the $US0.60s, as the gap between the RBA’s cash rate and the US Fed Funds rate pushes further into negative territory. Being short the $A remains a good hedge against things going wrong globally.

Eurozone shares rose 0.4% on Friday, but the US S&P 500 fell 0.7% with energy shares down 3.3% as the oil price continued to plunge. The weak US lead saw ASX 200 futures decline 37 points (or 0.6%) pointing to a weak start to trade for the Australian share market on Monday, with energy shares particularly likely to be under more pressure.

Leave A Comment