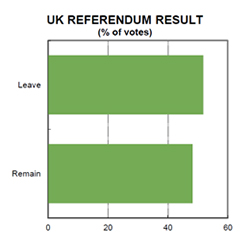

Britain has voted to ‘Leave’ the European Union (EU) 52 – 48 per cent. But the debate about the implications for economies and financial  markets is just beginning.

markets is just beginning.

The magnitude of the impact on markets and economies is open to debate. The likely rolling series of “shocks” are expected to be financial, political and economic. The UK will be most affected. But Europe (and the rest of the world) will not emerge unscathed.

A financial shock

Volatility has risen in the wake of the Brexit decision. Currency volatility can be seen in the Pound, US dollar and Australian dollar. We anticipate it will take up to another week before currency volatility settles down.

Standard & Poor’s indicated that a Brexit vote will see the UK lose its AAA rating. We expect the UK Gilt curve to steepen as investors leave the AAA (now AA). We don’t see the banking system as being as exposed to risk as it was during the GFC or various crises since then. Regulators and central banks are now well practised in providing liquidity during market disruptions.

The financial impacts will flow beyond the pure market reaction. Brexit will mean, for example, that the UK will lose its seat at the table when it comes to negotiations on European regulation and supervision (even as they still have to comply with many of those rules to do business in the EU). The risk of less market-friendly outcomes lifts as a result.

A political shock

With a Brexit, political casualties were inevitable. Britain’s Prime Minister David Cameron has resigned after the ‘Leave’ vote. Former Mayor of London, Boris Johnson responded by thanking Mr Cameron and saying, “There is no need for haste, nothing will change in the short term”.

The rest of Europe won’t escape unscathed. An Ipsos MORI poll published in early May surveyed voters across Belgium, France, Germany, Hungary, Italy, Poland, Spain and Sweden. Some 45% thought their own countries should hold a referendum on EU membership. And 33% indicated that they would vote to leave.

A confidence shock

UK household and business confidence was under some downward pressure as uncertainty increased and polling day neared. Further declines are likely as the complexity and difficulties associated with Brexit become clearer. European sentiment would be affected as well. The long timeframe for an exit means that confidence headwinds could persist for an extended period.

An economic shock

The main argument against Brexit was the potential economic costs. These costs are difficult to estimate. But all the serious modelling work suggests the impact will be large and long lasting.

In the short term, there is a significant risk that the UK economy slides into recession later in 2016 and 2017. The negative impact on activity from the confidence shock would be accentuated by a tightening in UK financial conditions. A UK recession would dent the already fragile growth prospects in Europe as well.

The longer-term cost to the UK economy comes from higher trade costs and less favourable trade access. A smaller-than-otherwise capital stock and labour force, and an erosion of skills, means the UK’s potential growth rate will step down.

Brexit and Australia

The general consensus is that the direct impact of Brexit on Australia will be fairly limited. Research shows Australia is less exposed than other countries to UK/European problems, partly because of our Asian orientation. While the real economy may escape relatively unscathed, the main danger may be to the income side of the growth equation.

Brexit will add to general market volatility and would see the AUD and interest rates move lower. These moves, especially the lower Aussie dollar, would provide some protection to the Australian economy.

Australian banks direct exposure to UK and Europe is significant. According to the RBA, the exposure of Australian-owned banks to the UK and Europe amounts to 25% of international exposures and 7% of global consolidated assets (as at the end of 2015).

RBA commentary on Brexit has been very limited. It is not mentioned in the March Financial Stability Review and gets only one mention in the May Statement on Monetary Policy and one mention in the Minutes of the July Board meeting. Nevertheless, the potential Brexit economic fallout would add to the RBA’s easing bias.

The UK, Europe and opportunities for Australia

There are some more medium-term opportunities for Australia from the Brexit vote. These opportunities lie with any re-orientation in UK trade and investment flows.

A shift in UK trade focus towards Asia, for example, could see a reversal of business platform flows. Instead of Australian companies using the UK as a springboard into Europe, UK companies may view Australia as a platform for launching into Asia.

The UK has always been a significant investor in the Australian economy. They remain the second largest foreign investor. Again, Australia could benefit from any redirection of UK foreign investment flows away from Europe.

A banking shock?

The Brexit win has negative consequences for UK banks and to some degree EU and US banks that base themselves out of London. But we regard the situation as quite manageable.

The lengthy exit process means lending volumes are likely to suffer as uncertainty around trade relationships and growth limit confidence. The lower interest rate environment will see margins pressured.

Lower GDP growth and rising unemployment typically points to higher credit costs. However, this is unlikely to be dramatic as UK banks are coming from a position of relative strength.

Operational challenges will present themselves in relation to London’s standing as a financial hub, which may see firms relocate to the Continent, presenting sizeable one off costs.

The rating agencies have indicated a double notch downgrade is coming to the UK sovereign rating (from AAA to AA). But we do not see an imminent threat to UK bank ratings, ie the sovereign downgrade is not a trigger for immediate downgrades to UK banks. None of the UK bank’s ratings include any uplift on account of implied government support.

Leave A Comment