A market update with Robb Hogg, Chief Investment Officer of SG Hiscock & Company Limited. This article delves into the key market movements, investor sentiments, and economic indicators that defined July, offering a comprehensive overview of how these factors shaped expectations for future monetary policies.

View this email in your browser

A month of heightened expectations.

July was a month of “rotation” in equity markets, weaker commodity prices, and further easing in global inflation pressures. This shifting dynamic resulted in rising hopes across the globe for policy rate reductions.

Over the month, global equity market performances were generally positive (notably except for the US NASDAQ), and market interest rates declined with falls more pronounced for shorter-dated securities (2 year bonds) than for longer term bonds (10 and 30 year bonds) as hopes for monetary easing gathered pace. The Australian dollar (AUD) slipped slightly against the US dollar.

Key market movements over the month were as follows:

• S&P/ASX300 Accumulation Index (i.e., including dividends) rose 4.1%.

• S&P/ASX Small Ordinaries (Australian Small Companies) Accumulation Index rose 3.5%.

• US equity market (S&P500) rose 1.1%.

• Australian 10-year bond yield slipped from 4.31% to 4.12%.

• Australian 3-year bond slipped from 4.09% to 3.76%

• The US 10 bond yield fell from 4.398% to 4.03%.

In July, increasing market confidence that the US central bank will begin cutting interest rates, perhaps as early as September, contributed to a change in equity market internal dynamics and a rally in bond prices (lower yields). The combination of further slowing in US inflation momentum and most US economic activity indicators drove this evolution in market dynamics.

In Australia, it was not until the last day of the month that a better-than-feared June quarter Consumer Price Index (CPI) report suggested that the RBA may also be able to move rates lower (rather than higher if the CPI had been stronger). Although the timing of rate cuts here is more uncertain than in the US, Australian market pricing implies a full 0.25% cut by February 2025.

Significant rotation in equity markets as US “Magnificent 7” stocks disappoint and monetary policy expectations evolve.

During the month the US equity market displayed a sharp reversal of fortunes with the so-called “Magnificent 7” recording sharp intra-month falls in their share prices. Some of this rotation seemed to reflect some disappointment with company quarterly reports, but some also seemed to reflect heightened expectations for near-term US central bank rate cuts. Rate cuts are usually regarded as particularly supportive for smaller companies (more so than for the large tech stocks).

Over the month the share prices of a number of the so-called ”Magnificent 7” stocks fell including Nvidia (down around 5.3%), Microsoft (down 6.4%), Meta (down 5.8%), Alphabet (Google) (down 5.8%) and Amazon (down 3.2%). Falls in these stocks were associated with a fall of -0.75% in the NASDAQ index.

Smaller companies were a key beneficiary of the rotation with the US Russell 2000 index rallying 10% over the month.

At its policy meeting on the last day of July, the US Federal Reserve (unsurprisingly) left policy rates unchanged (in the range 5.25% to 5.5%) and reinforced the increasing consensus that they will likely cut in September, conditional on continuing progress on reducing inflation and stable economic activity.

In the press conference following the meeting, Chair Powell noted that “The broad sense of the Committee is that the economy is moving closer to the point at which it will be appropriate to reduce our policy rate”. Powell also made the point that he “could imagine a scenario in which there would be everywhere from zero cuts to several cuts depending on the way the economy evolves”.

Moves to cut US official rates will remain data-dependent, but the market is already priced for cuts at each of the three meetings to come this year – September, November and December.

In particular, pricing will evolve according to developments in employment and inflation.

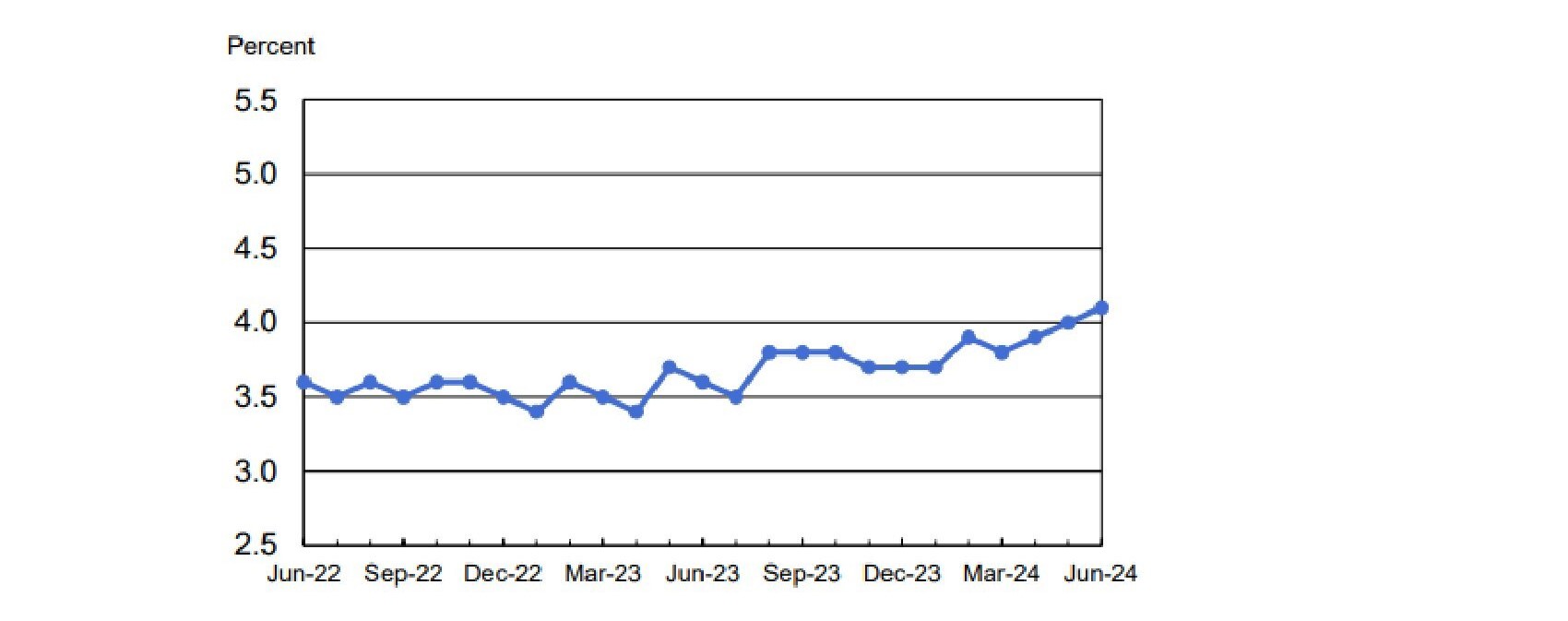

US June employment report suggests a gentle slowing in labour market conditions.

The June employment (non-farm payroll) report pointed to continued gentle slowing in US labour market conditions. Total US (non-farm) employment increased by 202,000 while the unemployment rate was unchanged at 4.1%.

US unemployment rate (June 2022 – June 2024)

Source: https://www.bls.gov/news.release/pdf/empsit.pdf

Source: https://www.bls.gov/news.release/pdf/empsit.pdf

Another mid-month downside surprise in the US CPI moves interest rate expectations further towards rate cuts.

Released mid-month, the latest US June Consumer Price Index (CPI) was lower than expected for the second consecutive month. The CPI index fell by 0.1% in the month, following no change in May. Underlying (core) inflation rose just 0.1% following a 0.2% increase in May.

Monthly change in the US CPI (June 2023 – June 2024)

Source: https://www.bls.gov/news.release/pdf/cpi.pdf

Again, it was important that underlying measures of inflation improved, such as those produced by the Federal Reserve Bank of Cleveland that measure “median” and “trimmed mean” inflation. These are measures that give a read on the breadth of inflation, and both suggested a continued easing in broader inflation pressures in the US economy as exhibited by slowing rates of monthly growth.

From a monetary policy standpoint, the ongoing easing of underlying inflation pressures is extremely positive as it is an easing in inflation momentum (if it continues) that will enable the US Fed to cut rates if economic growth continues to soften, as was highlighted by Fed Chair Powell at the July 31 meeting.

In contrast to what most central banks are doing, the Bank of Japan (BOJ) raised rates slightly in July.

As generally expected, the BOJ continued its policy normalisation process in July, raising the short-term policy rate from a range of 0%-0.1% to “around 0.25%”. As well, the BOJ announced plans to steadily reduce monthly bond purchases from around JPY 6 trillion to just under JPY 3 trillion by Q1 2026. The Yen rallied over the month in expectation of this further step in the policy normalisation process.

Chinese economic data weaker over the month.

Data released in China in recent months has generally surprised with its weakness. Consistent with this weakness was the release of China’s NBS manufacturing Purchasing Managers’ Index which declined further in July, from 49.5 to 49.4, marking a third consecutive month of contraction. New orders and new export orders underscored continued weakness in both domestic and foreign demand conditions. Meanwhile, the NBS services PMI slipped lower to 50.2 from 50.5, below expectations.

In response to continued signs of economic weakness, authorities announced additional measures to support consumption with a CNY 300 billion durable goods/equipment trade-in program. This followed two rounds of rate cuts earlier in the month.

Australia – most activity indicators and inflation are now easing, while employment remains surprisingly robust.

June quarter CPI was the key release in the month

Released on the last day of the month, the June quarter CPI rose by 1% taking annual inflation higher from 3.6% to 3.8%. However, of more importance than the headline number was the increase in underlying measures in the June quarter CPI. The increase in these underlying measures was less than feared. In particular, the key “trimmed mean” and the “weighted median” measures of inflation each recorded lower-than-feared increases of 0.8% in the quarter, taking their annual rates of change to 3.9% and 4.1% respectively.

This outcome quelled fears of the RBA needing to raise rates in August. However, inflation pressures are not yet completely vanquished as evidenced by the fact that “non-tradables” inflation (which includes goods and services that are mostly influenced by domestic factors) is still running at 5%, unchanged from the March 2024 quarter. Price rises for new dwellings, rents, tobacco and insurance all contributed to the annual rise.

Ongoing sizeable increases in these prices makes the policy decision difficult for the RBA as price rises on these types of goods and services are not easily damped by high interest rates. But the continuation of prices rises of this magnitude in domestically influenced non-tradeable goods and services runs the risk of unanchoring inflation expectations. Downward moves in this measure of inflation will be required before the RBA can begin cutting rates.

Australian employment data surprised on the upside again in June.

Employment growth remains the stand-out area of strength in the Australian economy. In yet another employment-related upside surprise, the number of people employed increased by another 50,200 in June which contributed, along with a small 9,800 rise in the number of people unemployed, to a slight rise in the unemployment rate to 4.1% from 4.0%. Measured on a trend-basis, employment is still increasing by 42,300 per month with the number of people employed rising by 2.8% since June 2023.

Australian employment (June 2014 – June 2024)

Source: https://www.abs.gov.au/statistics/labour/employment-and-unemployment/labour-force-australia/latest-release#media-releases

End-of-financial year sales boosted spending in June.

Australian retail turnover rose 0.5% in June following a 0.6% increase in May 2024 and a 0.2% rise in April 2024. Sales and discounts appear to be playing a key role in these increases.

According to the ABS, “End-of-financial year sales boosted spending in June by more than usual, particularly on discretionary items like furniture, electrical goods and clothing”. “Retailers told us that consumers continued to target sales events and look for the best deals before buying big-ticket items like furniture, bedding, TV’s and laptops,”

Retail trade (value) – June 2019 – June 2024

Source: https://www.abs.gov.au/media-centre/media-releases/mid-year-sales-boost-retail-turnover

Australian household spending skewed towards non-discretionary items.

The ABS reported in their latest Monthly Household Spending Indicator (an experimental indicator of household spending using bank transactions data), that household spending in May continued to be biased significantly toward non-discretionary spending. Over the year to May:

• non-discretionary spending rose 1.8%, driven by increased spending on health and on the purchase and operation of vehicles.

• discretionary spending fell by 1.9%, driven by decreased spending on clothing and footwear and accommodation services.

This dispersion in spending patterns is similar to the pattern exhibited by the ABS’s retail sales release and National Accounts whereby the rising cost of non-discretionary goods and services is diminishing the ability for consumers to spend on discretionary goods and services – such as alcohol and tobacco; clothing and footwear; furniture, floor coverings and household goods.

Non-discretionary and discretionary household spending (May 2020 – May 2024)

Spending on goods versus services is similarly bifurcated with annual household spending on:

1. services rising by 2.3%, driven by increased spending on health and other services.

2. goods falling 2.5%, pressured by decreased spending on clothing and footwear and goods for recreation and culture.

Goods and Services household spending (May 2020 – May 2024)

Source: https://www.abs.gov.au/statistics/economy/finance/monthly-household-spending-indicator/may-2024

Evolving expectations about monetary policy will continue to drive markets

As we have noted previously, evolving investor expectations about future central bank policy actions will likely continue to be the most important driver of market performances.

Market sentiment has shifted dramatically since the start of the year.

At the start of the year the market was expecting a benign outlook of slowing inflation and growth, allowing central banks to cut interest rates so cementing a “soft-landing”.

But soon after the year began, with investors noting the unexpected resilience of growth and inflation, expectations evolved to forecasts of “higher-for-longer” policy rates. The last month has witnessed expectations revert to where they were at the beginning of the year – an expectation of policy easing and a soft economic landing. The latest CPI release in Australia has likely put the RBA also on a path for rate cuts, but these may take longer to materialise as, although inflation and growth momentum are slowing, inflation pressures are easing only slowly.

August is reporting season

August is one of the two key reporting periods for Australian listed companies. Over the next few weeks investors will be looking for direction from companies regarding how much (or little) the RBA rate hike cycle has impacted demand and margins.

Leave A Comment